.svg)

Why Stablecoins Just Hit $320 Billion While the Rest of Crypto Fell 20%

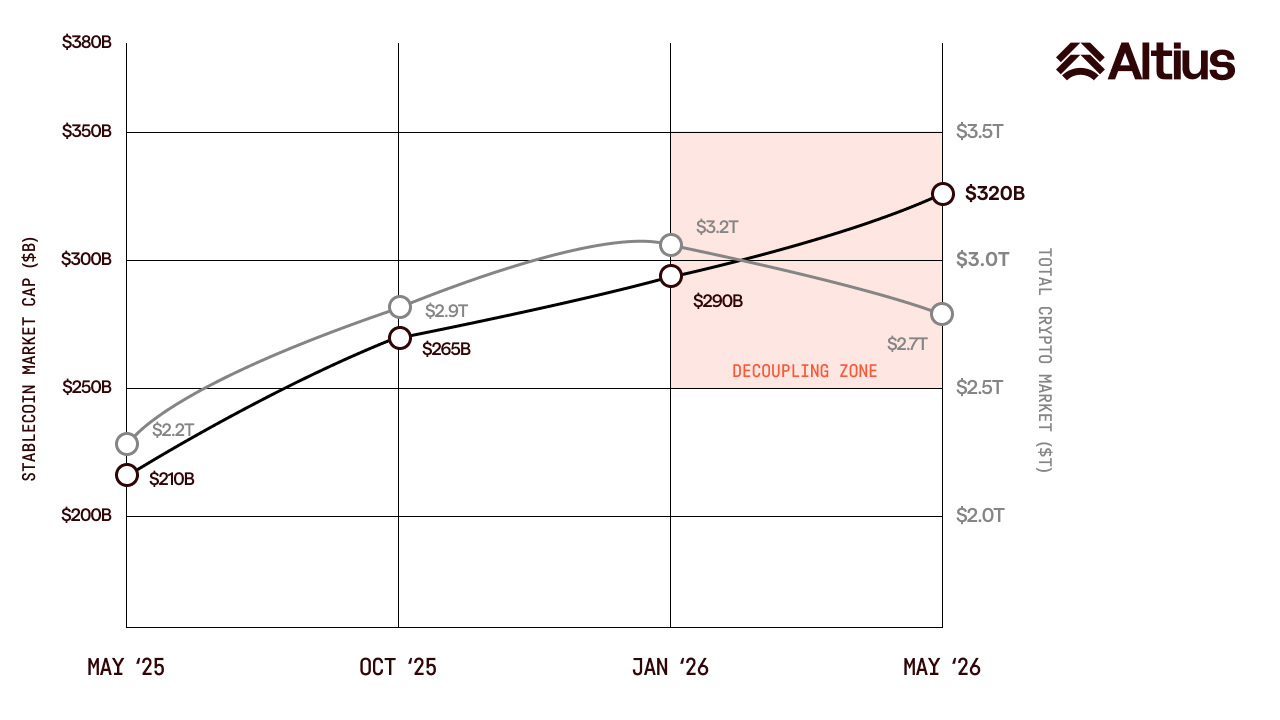

When the total stablecoin market cap crossed $320 billion in April 2026, it did so during a quarter where the broader crypto market lost more than 20% of its value, and that divergence is the most important part of the story. Unlike the retail-driven spikes of previous cycles, the momentum behind this milestone is being fueled by multi-billion dollar inflows from traditional finance institutions. That shift has been building for several years, and the Q1 2026 data has made it difficult to interpret any other way. Stablecoins have moved from a crypto-native instrument into general-purpose settlement infrastructure for a growing share of global financial activity.

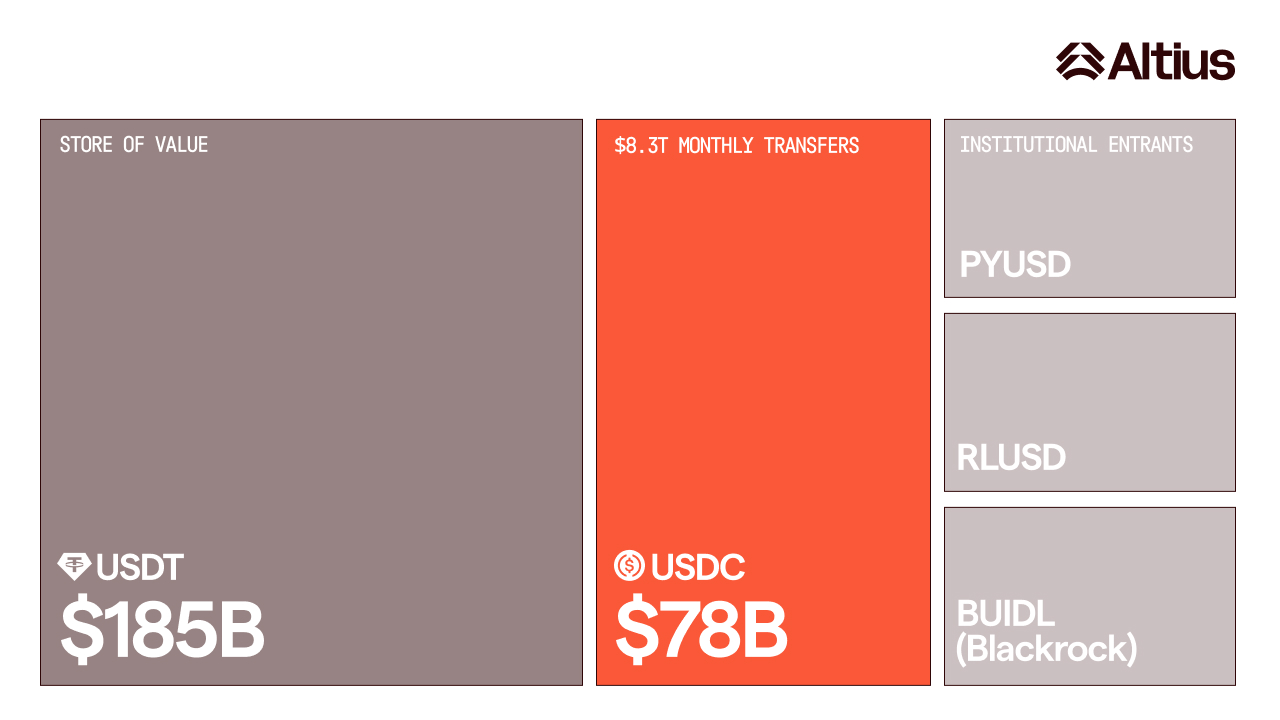

The issuer landscape reflects that shift clearly. USDT maintained a 58% market dominance at $185 billion while USDC reached approximately $78 billion by the end of April 2026, with institutional rotation toward regulated assets driving much of the divergence between the two. New entrants from major payment companies and asset managers crossed into multi-billion dollar territory inside of a year. The competition among issuers has become as much about regulatory credibility and reserve transparency as it has about market share, which is itself a signal of how far the market has matured.

Stablecoin Volume Hits a New All-Time High

Total stablecoin transaction volume hit $4.5 trillion in adjusted raw payment volume in Q1 2026, and a new all-time high, even as retail-sized transfers declined 16% in the same period, the steepest single-quarter drop on record. Volume rising sharply while retail activity falls is not a pattern you see in speculative markets. It points to a base of larger institutional flows that is growing independently of the retail participation that drove earlier cycles. B2B stablecoin payments grew from under $100 million monthly in early 2023 to over $6 billion by mid-2025, and that trajectory has continued through the first half of 2026 across cross-border payments, treasury operations, payroll, and vendor settlement.

Geographic adoption extends well beyond the US and European markets that have dominated coverage. Across Latin America, Southeast Asia, and parts of Africa, the cost and friction of correspondent banking has made the case for stablecoin settlement straightforward for businesses that traditional financial infrastructure has failed to serve. In EY-Parthenon's 2025 survey, 54% of non-using corporates and financial institutions expected to adopt stablecoins within six to twelve months, and based on the Q1 2026 volume data, a significant portion of those intentions have converted into active deployment.

Institutional Adoption Has Moved Past the Pilot Stage

What changed between 2024 and now is not the technology, which has been capable of handling institutional volume for some time, but the combination of regulatory clarity and competitive pressure that has pushed institutions from internal experimentation into production deployment. Regulatory frameworks across the US, EU, Hong Kong, and Singapore have established the baseline that compliance teams need to sign off on deployments, and the result has been a wave of integrations that would have been difficult to imagine two years ago. Traditional payment rails and broker-dealer platforms are now enabling customers to fund accounts and settle transactions using stablecoins, and the direction of travel is clearly toward deeper integration rather than parallel experimentation.

The competitive dynamic is also accelerating the timeline. When major card networks, payment processors, and financial institutions all begin moving stablecoin settlement from pilot to production within the same twelve-month window, the institutions that have not yet made that transition face a different kind of pressure than they did when the technology was still being evaluated. The $320 billion milestone is partly a function of genuine utility growth, and partly a function of institutions recognizing that the window for being an early mover is closing.

A $1 Trillion Market Cap Is Being Projected

Stablecoin circulation is projected to exceed $1 trillion by 2027, which would represent a tripling of the current market cap within a single year, and while projections at this scale carry obvious uncertainty, the direction is supported by the institutional deployment pipeline that is already visible in Q1 data. The businesses driving that growth are not moving capital through stablecoins because the technology is interesting. They are doing it because the economics of settling value through programmable, borderless, 24/7 infrastructure are materially better than the alternative for a growing range of use cases.

What that growth requires from the infrastructure layer is a different question, and one that gets less attention than the supply and volume numbers. Every institution that moves from pilot to production at meaningful scale has to answer questions about compliance enforcement, network ownership, finality guarantees, and how much control they actually retain over the settlement infrastructure they are depending on. Those are the questions that determine whether the $320 billion milestone is the beginning of a durable shift or a ceiling that the current infrastructure cannot push past.

At Altius, that is the part of the story we work on: building the chain infrastructure that gives institutions the performance, compliance architecture, and network ownership they need to operate at the scale the market is moving toward. The milestone is real. Making sure the foundation underneath it is built to match it is where the work actually happens.